Down to the penny budgeting is exceptionally difficult to stick with over the long-term. In fact for a lot of us "Budget" is nearly a four letter word. Instead this System uses buckets designed specifically to reduce the mental load of tracking every transaction while ensuring your financial goals are met automatically.

The Framework - Your monthly take-home pay will be divided into three primary buckets to ensure all bills are paid, savings are automated, and spending is controlled without the need for constant tracking.

Rule #1 - Give every dollar a job. Know what your money is for and make sure it goes where you want it to go.

Rule #2 - Let the computers help you. Automate, automate, automate.

Rule #3 - Multiple accounts actually helps make this work over the long-term.

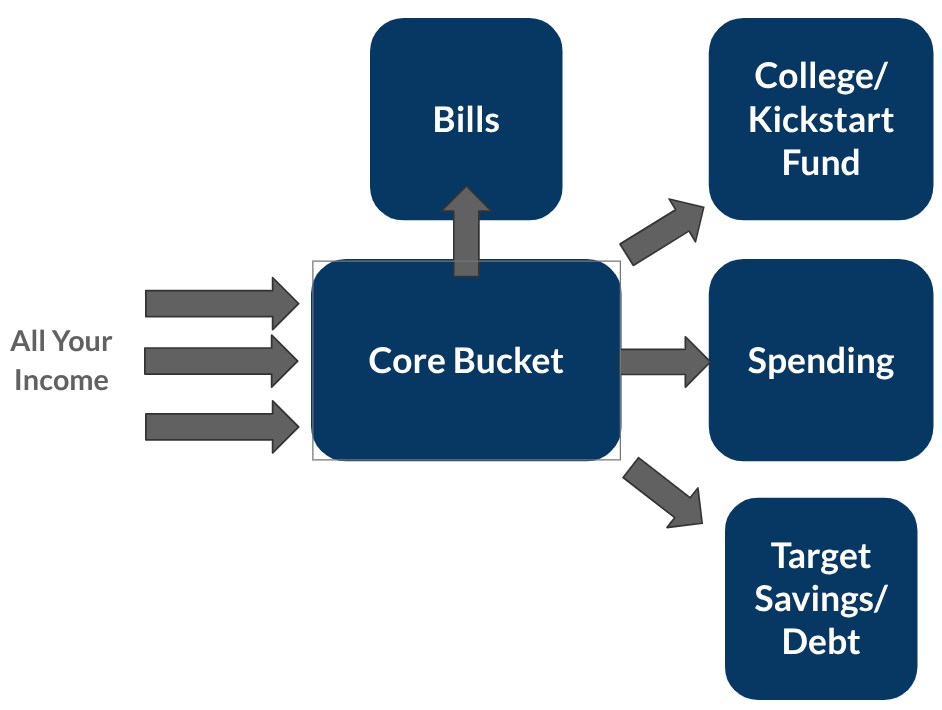

It looks a bit like this…

It does take a bit of time to set-up and get used to, but after 2-3 months it becomes smooth sailing for most families.

This comes to life when we walk through a simple example. Your values will of course be your own, but this can give you a good idea as to a good starting point.

1. Core Bucket (The Hub)

Account Type: Joint Checking - Monthly Inflow: $10,000

- The Job: This is "Grand Central Station." All income lands here. On the day after your paydays, automated transfers move money out to your other buckets.

- The Rule: You do not carry a debit card for this account. It is strictly for automated drafts.

2. The Bills Bucket (~40%)

Account Type: Not Really a Stand-Alone Account Actually - Allocation: $4,000

- The Job: This bucket is for your "Static" life—the things that don't change much month-to-month.

- What it covers: Mortgage, Utilities, insurance premiums, car payments, and subscriptions.

- Execution: Set all these bills to Auto-Pay directly from the Core Bucket account. We call this a Bucket, but it’s not a separate account, but the amount that we expect to go our consistently for those “Fixed” things.

- The Rule: You do not carry a debit card for this account. It is strictly for automated drafts.

3. The Spending Bucket (~40%)

Account Type: Joint Checking - Allocation: $4,000

- The Job: This is your "Variable" life. This is where most of your credit card "creep" currently happens.

- What it covers: Groceries, dining out, Target/Amazon runs, gas, and baby supplies.

- Execution: Move this $$$ to a separate checking account with its own debit card.

- The Rule: When this account hits $0, the spending stops until next month. If you prefer to use a credit card for rewards, you must pay it off weekly from this bucket only. If the balance exceeds the bucket, you are overspending.

4. The College/Kickstart Fund Bucket (~5%)

Account Type: Flexible (529, 530A, Brokerage, etc. ) - Allocation: $500

- The Job: Investing in your child/children's future.

- Execution: Automated transfer from the Core Bucket each month..

- The Rule: A “little” but consistent savings, especially when invested, can go a long way over time.

5. The Targeted Savings/Debt Bucket (~15%)

Account Type: Based on goal (HYSA for Emergency Fund or Travel or Brokerage Account for Sabbatical Fund) - Allocation: $1,500

- The Job: Big-ticket items and "Peace of Mind."

- What it covers: Those other goals like an Emergency Fund, Big Trip, Extra Debt Payoff, House Repairs, Sabbatical.

- Execution: By "giving these dollars a job" now, you won't feel the need to put a $2,000 emergency car repair on a credit card later.

What if your income isn't nice and clean on the month? Let's say like most you get paid every two weeks - plan your monthly in/out based on the 2 paycheck months and treat those 3 paycheck months like a bonus toward one of your goals. But how about income from bonuses, RSUs, etc.? Treat each one like a one-time event when it's coming up. Make a plan a head of time - where are going to put that money to work? And then make the transfers manually when they come in to the Core Bucket.

Again, this looks complicated and it does take a bit of time to setup and then 2 months or so to get used to, but like any system that actually works, it's worthwhile. Once it's up and running you don't need to keep tracking your spending or worrying if your money is going where it needs to to meet your goals - you've done the work already and now the system is doing it's job.