If you're working at Microsoft, your compensation package probably includes more than just your paycheck. Between Restricted Stock Units (RSUs), the Employee Stock Purchase Plan (ESPP), and your 401(k) options, there's a lot to keep track of. And honestly? It can feel overwhelming.

But here's the thing: understanding how these pieces fit together isn't just about maximizing dollars on a spreadsheet. It's about making smart decisions that align with the life you want to live—whether that's retiring early, funding your kids' education, or having the flexibility to take that career risk you've been thinking about.

Let's break it down in plain English.

Why Microsoft Uses Stock Compensation (And Why It Matters to You)

Tech companies like Microsoft lean heavily on stock compensation for a couple of good reasons. First, it creates alignment—when the company does well, you do well. Second, it helps with retention through vesting schedules. But for you, the real question is: how do I make the most of this?

Restricted Stock Units (RSUs): Your Biggest Compensation Component RSUs are probably the largest piece of your equity compensation puzzle. Here's how they work:

Microsoft grants you RSUs based on various milestones—when you're hired, as part of your annual compensation, or when you hit specific performance goals. These aren't actual shares yet; think of them more like IOUs that convert to real stock once they vest.

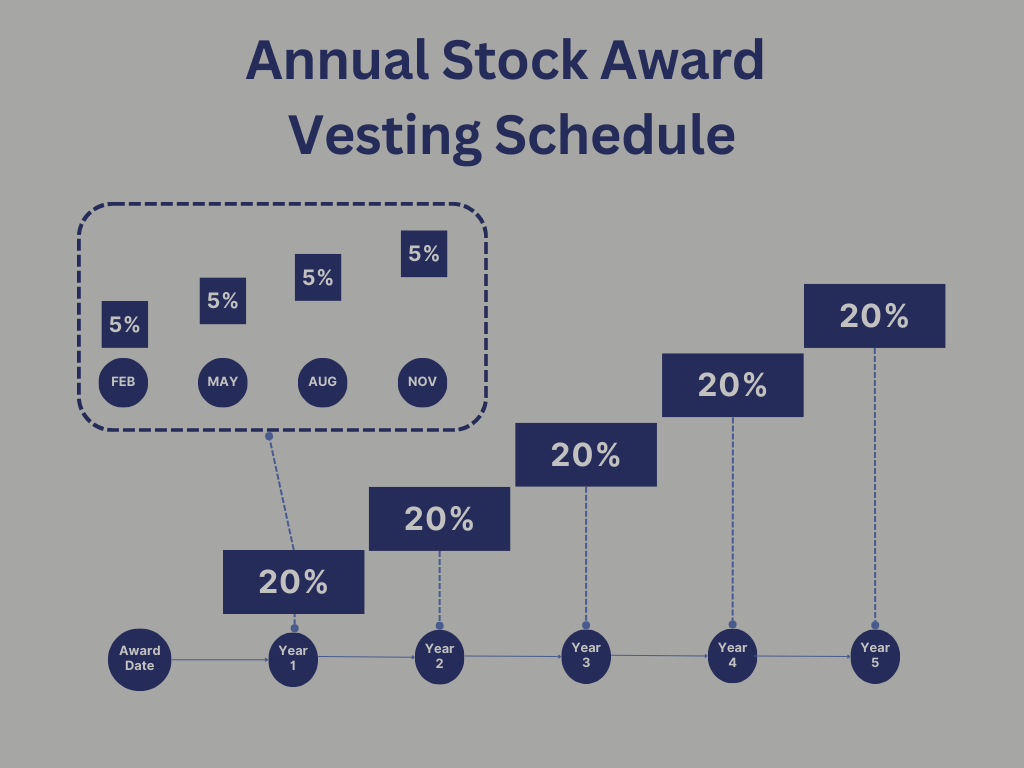

There are two main vesting schedules you need to know:

1. On-Hire Awards: Those RSUs vest 25% every year over the first four years with Microsoft. These shares vest on your employment anniversary (nothing to do with the calendar year).

2. Annual Award: In August of every year Microsoft determines an award of stock for each employee. The vesting schedule for these awards has its own rhythm. They vest 20% every year over five years, but in 5% increments each quarter.

The vesting schedule matters. Your shares vest over time, and when they do, you'll owe taxes. Microsoft will automatically sell some of your shares to cover the federal supplemental withholding rate of 22%. But here's the catch: that might not be enough if you're in a higher tax bracket. Plan accordingly so you're not surprised come tax time.

A special note for long-timers: If you hit 55 years old with 15 years of service (or reach 65), any stock grants older than one year will continue vesting even if you leave. That's a nice safety net worth knowing about.

The Employee Stock Purchase Plan (ESPP): A 10% Discount

Microsoft's ESPP lets you set aside up to 15% of your salary (after-tax) to buy Microsoft stock at a 10% discount every quarter. It sounds straightforward, and it can be a nice benefit—but it's worth thinking critically about whether it makes sense for your situation.

Diversification matters. If RSUs already make up a big chunk of your net worth, adding more Microsoft stock through ESPP might not be the smartest move. You don't want too much of your financial future tied to a single company, no matter how well it's performing right now.

But… one strategy to consider is to use this as a wealth stacker for your income today - set aside the 15%, get the 10% discount and sell immediately, grabbing that 10% as an extra bonus each quarter.

Don't Forget Your 401(k)

Your Microsoft 401(k) also gives you the option to invest in company stock. And if you've been with the company for a while, you might want to learn about Net Unrealized Appreciation (NUA) treatment—it's a tax strategy that can significantly reduce your tax bill on Microsoft stock held in your 401(k). It's complex, but for some people, it's worth exploring.

The Big Picture: Avoiding Overconcentration

Here's something we see a lot: engineers and tech professionals with portfolios that are way too heavy in their employer's stock. Between RSUs vesting, ESPP purchases, and 401(k) holdings, it's easy to end up with 50%, 60%, even 70% of your net worth tied to Microsoft.

That's risky—not because Microsoft isn't a great company, but because no one can predict the future. Remember, diversification isn't just about protecting against downside; it's about giving yourself options and flexibility in life.

What Should You Actually Do?

Here are some practical strategies worth considering:

Think about your cash flow differently. Instead of letting vested RSUs pile up while you cover expenses with your salary, consider the reverse. Live off your vesting shares and maximize your paycheck deductions for tax advantaged accounts. This can unlock some powerful tax-saving opportunities.

Have a diversification plan. As shares vest, consider selling some and reinvesting in a more diversified portfolio. Yes, you might miss out on gains if Microsoft keeps climbing—but you'll also protect yourself if things don't go as planned.

Coordinate your overall financial plan. Your Microsoft compensation shouldn't exist in a vacuum. It needs to work with your other goals: career changes, retirement planning, education funding, risk management, and everything else that matters to your family.

The Bottom Line

Your Microsoft compensation package is a powerful wealth-building tool. But like any tool, it works best when you understand how to use it—and when you use it in service of something bigger than just accumulating more stock.

Life doesn't follow a script. Your financial plan shouldn't either. Whether you're early in your Microsoft career or approaching that 55/15 threshold, the key is making intentional decisions that keep your plan aligned with your life as it changes.

Want to talk through your specific situation? That's what we're here for. No cookie-cutter approaches—just a real conversation about what makes sense for you.

The information in this post is for educational purposes only and should not be considered tax or investment advice. Everyone's situation is unique, and you should consult with qualified professionals about your specific circumstances.